FY24: Investment Process + Outlook

Update on my investment process, macro indicators, market, sentiment, and outlook

Investment Process Update

My initial investment philosophy when starting this blog was:

Markets, as social constructs, are influenced by investor expectations, fundamentals, and liquidity. Success hinges on accurately predicting changes in expectations and sizing positions correctly. Fundamentals provide insights into outcomes not fully appreciated by the market.

I have since updated my investment process to account for the following:

(1) Less prediction; more business cycle awareness: Don’t rely on timing the market

Change in newsletter: Business Cycle section

(2) Diversify and focus on risk management: Your objective is to survive long enough to make money. Diversify across ideas and don’t “lose the farm” on any single bet.

Change in newsletter: Market Update section

(3) Observe sentiment & investor positioning: Howard Marks believes deeply in the importance of market cycles, driven by the tendency of people to go to excess on both the upside and downside. We should monitor sentiment and valuations.

Change in newsletter: Sentiment section

TL;DR

Business Cycle

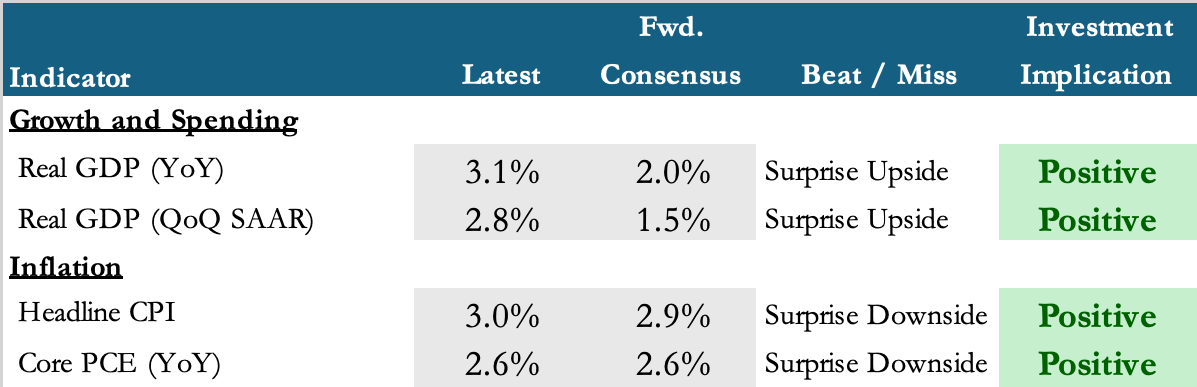

The economy appears to be in the late stages of the business cycle, characterized by (1) strong but declining growth; and (2) elevated but slowing inflation. In isolation, this would be a risk-off environment (bad for stocks). However, consensus forward estimates for growth and inflation appear soft relative to expectations, suggesting potential positive surprises in both areas in the medium term (good for stocks).

Outlook

The combination of both the factors above (positive expected beats on growth and inflation) is a positive setup for equities in the next 3 months. However, the rotation from growth to value this past week (see “Market Update” section) is likely to continue in the near-term so probably wise to hold some cash to buy dips until the volatility subsides.

Growth: The U.S. economy is showing above-trend growth. EY-Parthenon forecasts that GDP growth will exceed consensus estimates on Bloomberg. This higher-than-consensus forward estimate is positive for risk assets in the medium term.GDP growth was mainly driven by increases in consumer spending (+2.3%) and business investment (+5.2%) (Torry).

Corporate financial health is robust (Slok et al.), as evidenced by:

S&P 500 forward profit margins near record highs

Bank lending growing

Bankruptcy filings trending lower

Consumer spending is robust, with credit card spending, same-store sales, air travel, and restaurant bookings significantly above trend (Slok et al.).

Inflation: Inflation remains elevated but is moderating. Shelter costs, the largest component of inflation, are trending lower. As this trend continues, we expect inflation to fall below estimates. This lower-than-consensus inflation rate is positive for risk assets in the medium term.June inflation data indicated widespread cooling, with both shelter costs and goods prices declining for multiple consecutive months

Shelter costs, the largest component of CPI, rose at the slowest rate in 3 years

Core goods prices fell for a 4th straight month and services prices ex-housing declined for a 2nd month

Labor market conditions are improving (Initial jobless claims are trending downward; tax withholdings show stable income levels)

Market Update

Recent market trends show a rotation towards small-cap stocks

A rotation into small-caps started last week, with the Magnificent 7 losing nearly $2 trillion in market capitalization in 10 days

The Russell 2000 (small-cap index) has risen 12.3% year-to-date, nearly matching the Nasdaq 100's 13.4% gain ("#GLOBALMARKETS WEEKLY WRAP-UP")

The forward price-to-earnings ratio of the Nasdaq index at the beginning of July was about 35 times, versus just 16.5 times for the S&P 500 equal-weight index ("#GLOBALMARKETS WEEKLY WRAP-UP")

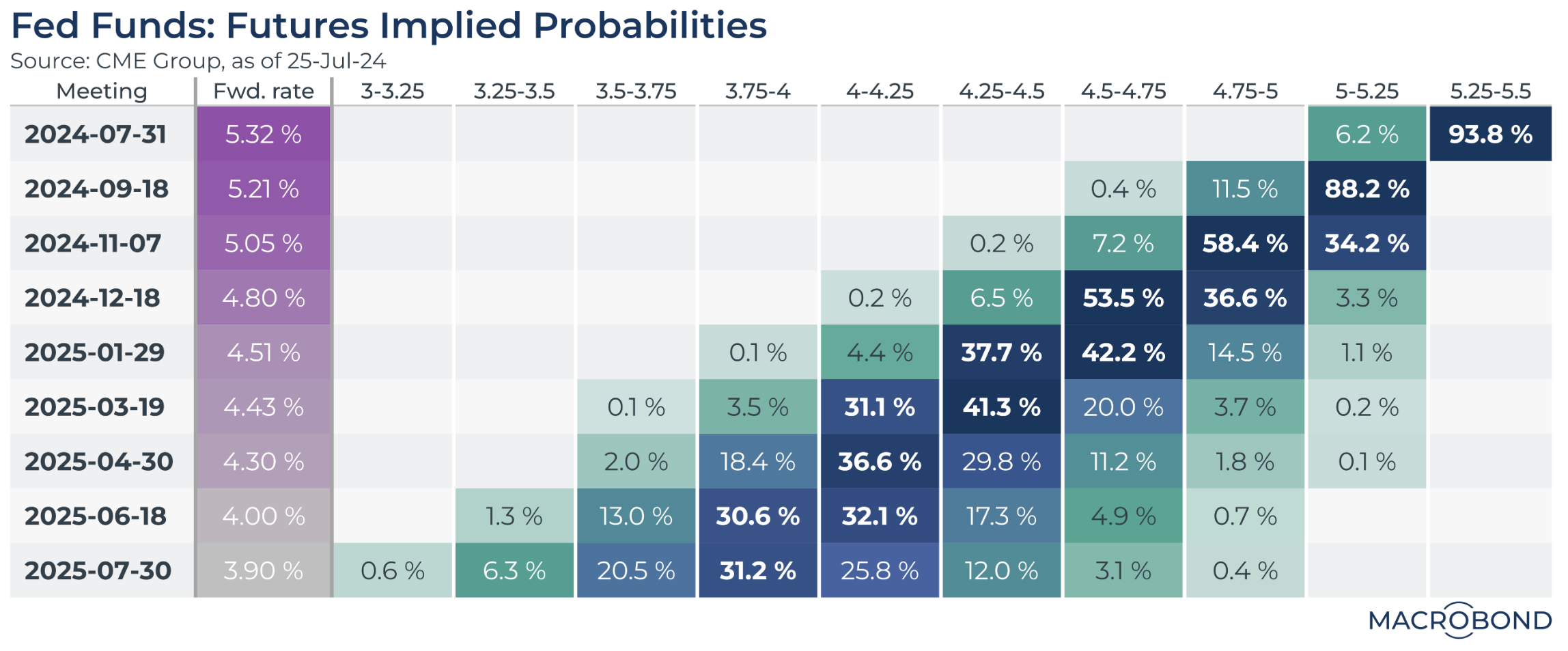

EY-Parthenon expects two 25bps rate cuts in 2024, likely in September and December, followed by 125 bps of easing in 2025 (Daco et al.). The market has already priced in these rate cuts into futures curves.

Sentiment

Sentiment can be measured using positioning studies and valuation metrics. By monitoring these indicators, we can gauge whether the market is overly optimistic or pessimistic relative to long-term averages.

AAII Bull-Bear Spread

NAAIM Exposure Index

The NAAIM Exposure Index represents the average exposure to US Equity markets. This weeks exposure is 76.70 (vs. 81.70 last quarter).

Valuations

Yardeni Research Valuations

Valuations for MegaCap stocks (30.0x P/E) are higher than long-term averages and materially higher than the rest of the market

A rotation into the Russell 2000 (small-cap index) has started to occur this past week (index up 12.3% year-to-date), partially because of the differential in valuation ratios (15.4x P/E vs. 30.0x for MegaCaps)

Detailed Observations

Growth

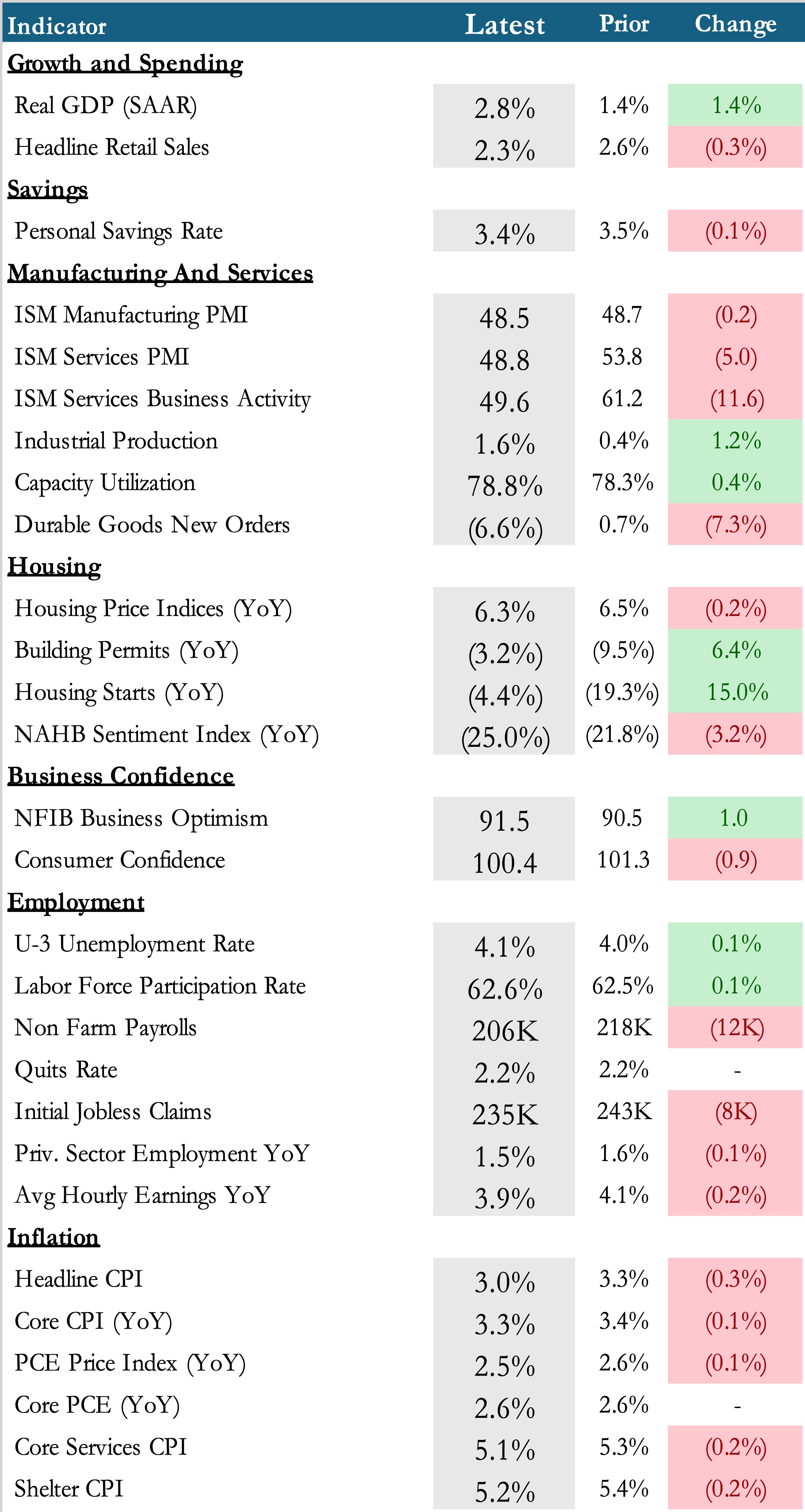

Overall economic expansion continues, with Real GDP accelerating to 2.8% (up 1.4%), driven by strong consumer spending and robust industrial production.

Manufacturing and services sectors show weakness, with both ISM Manufacturing (48.5) and Services PMI (48.8) in contraction territory, signaling potential broader economic slowdown. However we will receive updates to both of these readings in the coming weeks.

Business investment outlook is mixed, as evidenced by sharply declining Durable Goods New Orders (-6.6%, down 7.3%) contrasting with slightly improved NFIB Business Optimism (91.5, up 1.0).

Housing market indicates late-cycle dynamics, with volatile Housing Starts (-4.4% YoY but up 15.0% MoM) and weakening NAHB Sentiment (-25.0% YoY). The housing market is particularly sensitive to interest rates and often leads the broader economy, making it a key indicator to watch for potential economic shifts.

Inflation

Inflation is moderating but remains elevated, with Headline CPI at 3.0% (down 0.3%) and Core PCE steady at 2.6%, both above the Federal Reserve's 2% target.

Headline PCE inflation decreased to 2.5% year-over-year, the lowest level since February 2021

PCE Shelter Inflation (Green Line) has fallen from 5.7% (Mar-24) to 4.5%

PCE Services Inflation ex-shelter and energy (Red Line) is declining as well, which is a good sign as it is a key input for the Fed's policy decisions.

Labor / Wages

Labor: The labor market is cooling gradually without severe disruptions

Despite job postings declining 12.4% year-over-year, the unemployment rate of 4.1% (up 0.1%) remains relatively low by historical standards.

Average Hourly Earnings growth at 3.9% YoY (down 0.2%), suggesting potential easing of wage-driven inflation pressures.

Steady Quits Rate (2.2%) and slightly improving Labor Force Participation Rate (62.6%, up 0.1% and below pre-pandemic levels).

Tax withholdings show no signs of slowdown, suggesting stable employment and income levels (Slok et al. 12).

Upcoming Releases: The Treasury and jobs data (along with Mag7 earnings) may cause some stock market volatility in the near-term.

Jobs market data

JOLTS job openings (Tuesday)

ADP private payrolls (Wednesday)

Weekly jobless claims (Thursday)

Nonfarm payrolls for July (Friday)

Economic indicators

July Conference Board consumer confidence (Tuesday)

ISM manufacturing index for July (Thursday)

Treasury

Announcement of quarterly refunding plans & auction (Monday)

$70 billion in 42-day bills (Tues)

Sentiment

Sentiment

Accoring to the AAII Investor Sentiment survey, investors were more bearish this week (31.7% vs 23.4% previously)

Allocation

Largely overweight stocks (70.5%) and underweight cash (15%)

The NAAIM Exposure Index represents the average exposure to US Equity markets. This weeks exposure is 76.70 (vs. 81.70 last quarter).

Valuations

Yardeni Research Valuations

Valuations for MegaCap stocks are higher than long-term averages and materially higher than the rest of the market

A rotation into the Russell 2000 (small-cap index) has started to occur this past week (index up 12.3% year-to-date)

Market Update

The 'Magnificent 7' stocks lost ~$2 trillion in market capitalization over 10 days

4 out of 7 Mag 7 companies (NVIDIA, Amazon, Meta, and Alphabet) are expected to report year-over-year earnings growth of 56.4% for Q2-24 (vs. 5.7% for the remaining 496 companies in the S&P 500). The market's reaction to these earnings reports could significantly impact overall index performance, given the outsized weighting of these stocks on the index.

Nvidia earnings come out 8/28

Amazon earnings come out 08/01

Meta earnings come out 7/31

Alphabet net income rose 29% but stock is down 6% this week

Microsoft earnings come out 7/30

Tesla earnings missed by -16.15%; stock is down 8% this week

Value sectors are performing again

The Russell 2000 (small-cap index) has risen 12.3% year-to-date, nearly matching the Nasdaq 100's 13.4% gain ("#GLOBALMARKETS WEEKLY WRAP-UP")

The forward price-to-earnings ratio of the Nasdaq index at the beginning of July was about 35 times, versus just 16.5 times for the S&P 500 equal-weight index ("#GLOBALMARKETS WEEKLY WRAP-UP")

Liquidity

Markets are pricing in 2-3 rate cuts this year

Fed officials have signaled that a cut is "very possible" at their September meeting ("A Fed Rate Cut Is Finally Within View"), with some officials like Former New York Fed President Dudley signaling a cut as early as next week.

Powell has noted that because price measures lag behind economic conditions, waiting until inflation hits 2% to cut rates means "you've probably waited too long" ("A Fed Rate Cut Is Finally Within View")

Most likely outcome is first cut in September (88% probability). However, unexpected inflation or growth surprises could alter this timeline.

Bibliography:

"#GLOBALMARKETS WEEKLY WRAP-UP." Syz Group, 27 July 2024.

"A Fed Rate Cut Is Finally Within View." The Wall Street Journal, 28 July 2024.

Daco, Gregory, et al. "Executive Briefing: Macroeconomic Outlook and Impact on Businesses." EY-Parthenon, July 2024.

"Fed Is About to Nod at a Rate Cut as Job Growth Moderates." Bloomberg, 27 July 2024.

Nazareth, Rita. "Wall Street's Great Rotation Resurfaces After GDP: Markets Wrap." Bloomberg, 25 July 2024.

Saraiva, Augusta. "US Economy Grew Faster Than Expected Last Quarter on Firm Demand." Bloomberg, 25 July 2024.

Slok, Torsten, et al. "Daily and Weekly Indicators for the US Economy." Apollo Global Management, 27 July 2024.

Torry, Harriet. "Economic Growth Quickens, Rising at 2.8% Rate in Second Quarter." The Wall Street Journal, 25 July 2024.

"Why the Great Stock Rotation Is Skipping Consumer Staples." The Wall Street Journal, 27 July 2024.

William, Ron. "Real Vision Interview with Ron William." Real Vision, 18 July 2024.