My Investing Strategy

How I generated 173% cumulative returns over 4 years

Overview

I’m sharing my personal investment strategy using real trade examples—including painful failures. After four years of refinement, it’s finally working (see performance below). But the journey taught me as much through failure as through success.

This isn’t investment advice—it’s a transparent look at a systematic approach that has worked for me, including the mistakes that almost derailed it. Every trade shown is real—wins, losses, and the catastrophic mistakes when I broke my own rules. Your constraints, taxes, and risk tolerance may differ. I’ve shared real trades (both wins and losses) to illustrate the strategy in action, but past performance is not indicative of future results. Do your own research.

First, the scoreboard:

Four-Year Return: >100% cumulative outperformance vs. benchmark

One Year Return: ~2x outperformance vs. benchmark

The Framework: Macro-Driven & Regime-Based

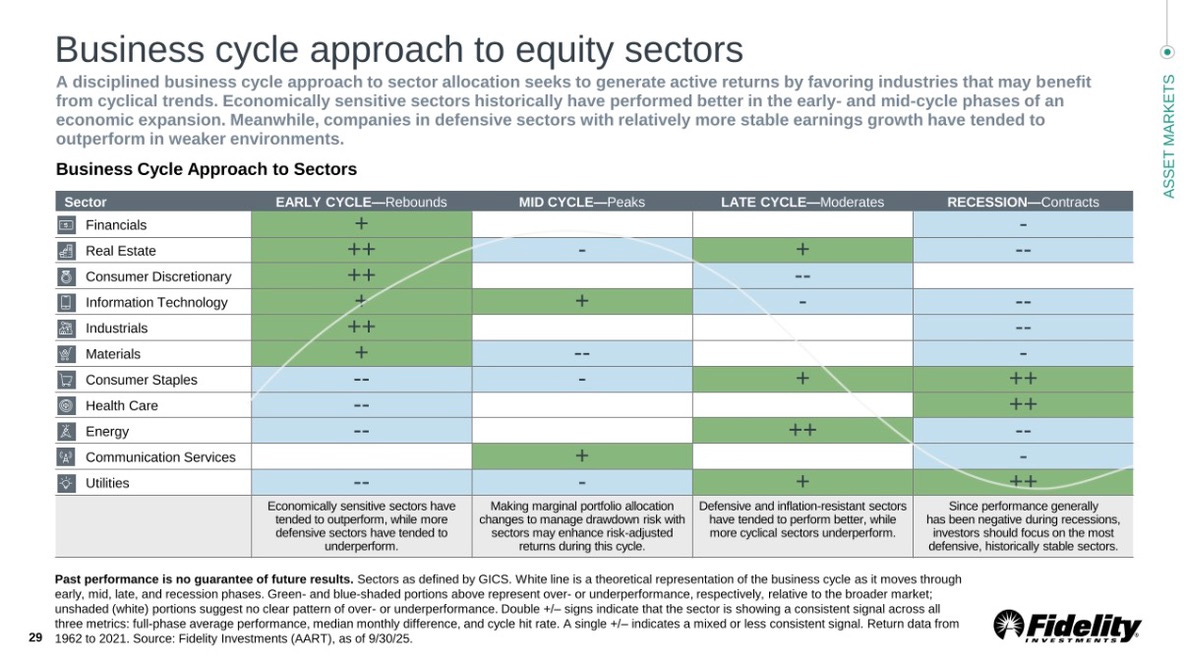

Core Philosophy: Markets are often inefficient around regime transitions—shifts in growth and inflation. I aim to capture that inefficiency using 42Macro’s framework. (See Appendix below for details)

My edge: Deciding how much risk to take, and in which assets, based on the macro regime. I express that view with low-cost index exposure, a small set of diversifier ETFs, and a tactical options overlay that deliberately targets higher beta (or risk) when conditions are favorable and prioritizes capital preservation when conditions are bleak.

In plain English: I buy assets that perform well in the current regime and cut exposure when conditions shift. I optimize for risk-adjusted return—specifically, return per unit of drawdown.

The Toolkit (6–8 liquid ETFs):

Equities: broad US beta (e.g., S&P 500 / Nasdaq)

Duration: short and long US Treasuries

Real assets/defensive: Gold

Alternative risk: Bitcoin (size capped)

Cash/T-Bills: dry powder and optionality

The Options Overlay:

Defined-risk options to lift portfolio beta to 1.5–3.0× in risk-on regimes; minimal or protective positions in risk-off.

North Star: Keep drawdowns shallow so compounding continues and discipline holds. I try to stay systematic (though I don’t always succeed, as you’ll see).

Why This Approach?

Know your statistical investing edge: Stock picking is hard and I’m not good at it. My skillset favors macro signals (not company-specific analysis).

Cost efficiency: Indexing (SPY, QQQ) plus a few diversifiers keeps costs low. The options overlay is systematic and defined-risk—not ad-hoc speculation.

Behavioral discipline: Rules reduce the chance I panic-sell or chase. Position bands, regime flags, and drawdown triggers keep my emotions in check.

Real Trade Analysis

Here are three strategies I’ve run—one correct, two wrong

SPLG index options (green) — The framework working

Individual stock picking (red) — Mistake #1

Crypto miner concentration (yellow) — Mistake #2

In each case I will show the returns + how I did on a risk-adjusted basis.

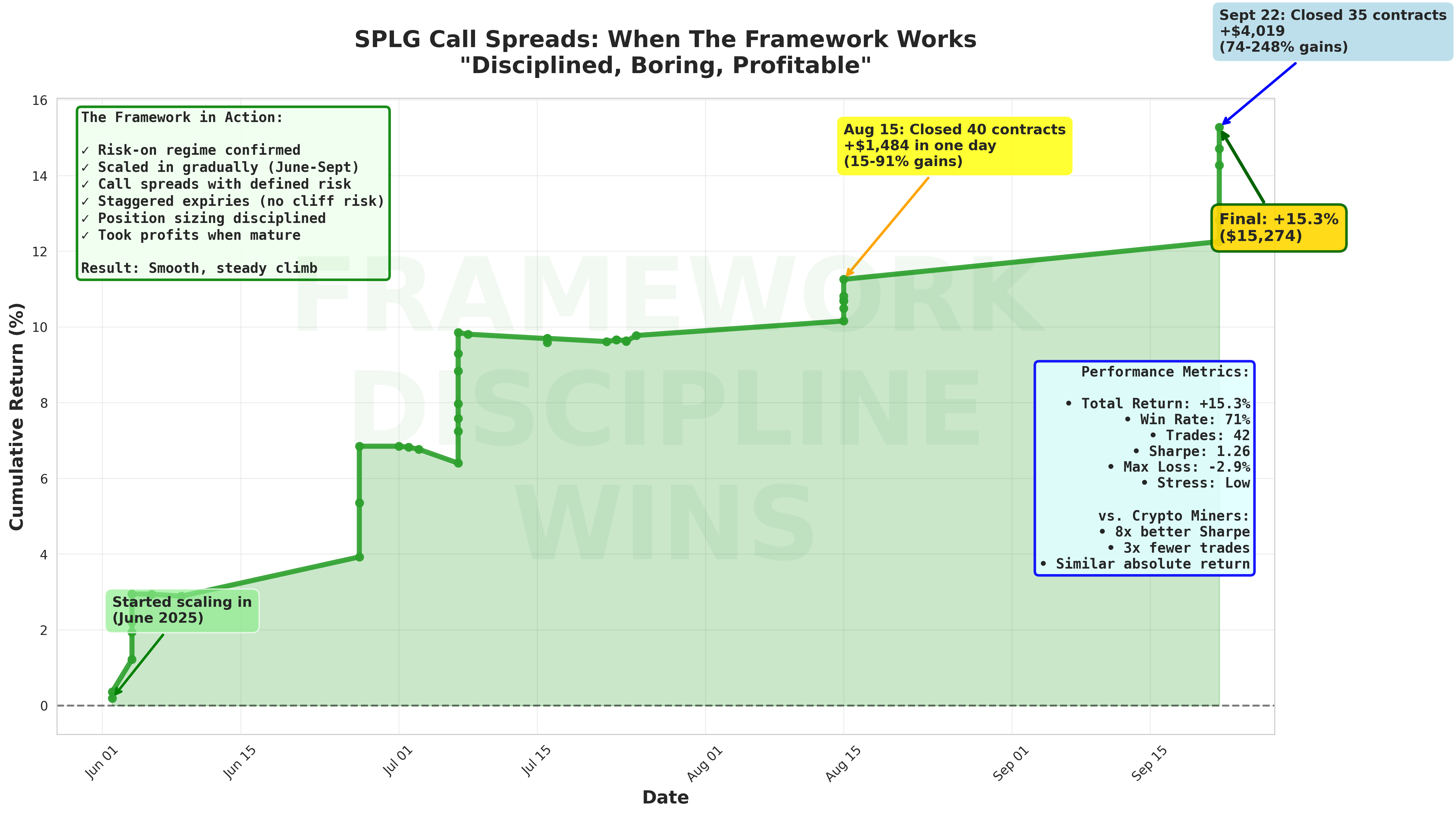

When It Works: SPLG Index Options

Context: In the Summer of 2025 my regime indicators aligned perfectly. Growth was stabilizing, inflation cooling, credit spreads calm, and equity trends positive. Textbook risk-on environment.

The execution: I opened a series of call spreads on SPLG (SPDR Portfolio S&P 500 ETF—essentially a low-cost S&P 500 index ETF) in addition to holding the underlying.

The results: Cumulative returns of >16% over a few months in SPLG alone

I didn’t go all-in. I scaled in as signals confirmed, staggered expiries (July, August, September, October), and kept each position under 2% of NAV in premium at risk

Why it worked:

Regime persistence: Once the risk-on signals aligned, they stayed aligned for several months

Defined risk: Every call spread had bounded loss (I knew exactly what I could lose)

Disciplined scaling: I didn’t chase. Each new position required the trend and volatility regime to stay supportive—or I exited.

Staggered expiries: I didn’t concentrate everything in one expiry (had July, August, September, October expiration dates on my options)

This is the strategy as designed. But following rules is easy when you’re winning. The real test? Let’s see what happens when you break them…

When I Broke My Own Rules

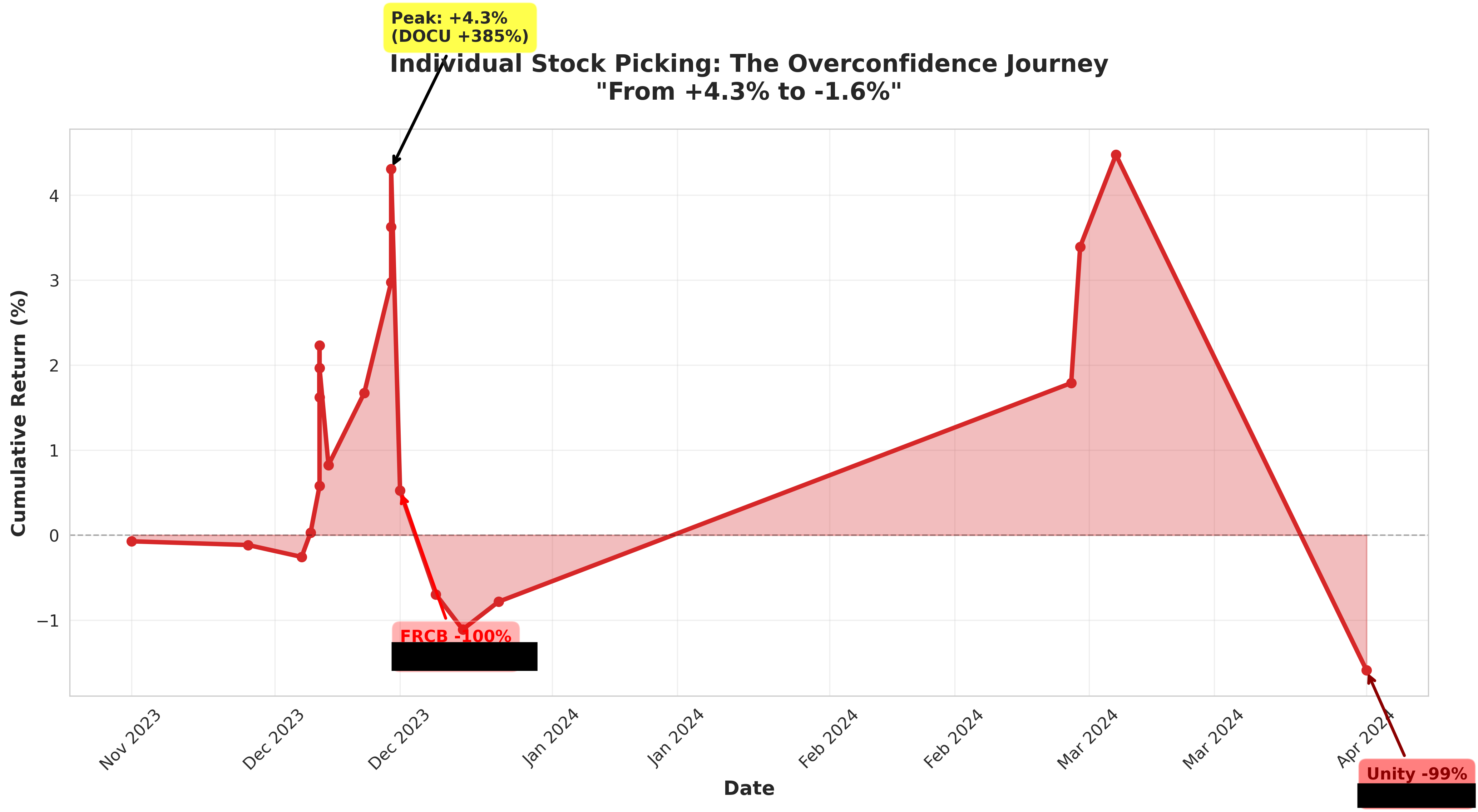

Mistake #1: Individual Stock Picking

What happened: Despite my framework explicitly rejecting stock picking, I convinced myself I had an edge (I did not, as I soon found out).

The trades:

DocuSign (DOCU): Nov-Dec 2023 calls. Made +148%, +166%, +385% on three positions—then gave it back.

Unity Software (U): Dec 2023-Feb 2024 calls. Near-total loss.

Block/Square (SQ): Multiple attempts, mixed results. Some +260% wins, one catastrophic loss.

First Republic Bank (FRCB): Company bankruptcy = total loss.

What I told myself: I had ‘high-conviction’ reads on idiosyncratic catalysts—DOCU’s earnings turnaround, Unity’s management change, Square’s undervaluation, regional banking overreaction.

Why this violated the framework: My edge isn’t company-specific analysis. The framework is explicitly built around regime-based allocation, not security selection. Even when some of these trades made money, they increased portfolio complexity, introduced single-stock risk, and pulled attention away from the macro signals that actually matter.

The lesson: When I stick to broad indices, no single name can blow up my portfolio (like First Republic Bank did in this instance). When I pick stocks, I’m competing with specialists who live inside those names. I don’t have an edge there.

Net impact: FRCB alone nearly wiped out all the wins. Even worse, the mental energy spent analyzing company stories was a complete waste relative to the returns.

Mistake #2: Crypto Miner Concentration

What happened: I went big on crypto miner options—HUT and RIOT—during Bitcoin’s 2023-24 rally. Made 14.7% but the risk-adjusted returns were terrible.

What my framework says: 0-5% Bitcoin via ETF, not individual miners.

What I did: The exact opposite. The wins felt easy.

What I told myself: Bitcoin was rallying in late 2023. I wanted leveraged exposure. Instead of sticking to spot Bitcoin (or IBIT/Bitcoin ETFs), I convinced myself that crypto miners were “cheap call options on Bitcoin.” I sized these positions far larger than my framework allows (multiple tranches, multiple strikes, too much risk).

Why this violated the framework:

Single-name concentration: HUT and RIOT are individual companies with operational, regulatory, and dilution risk—not diversified Bitcoin exposure

Excessive leverage: These were already volatile stocks; call options added another layer of leverage

Position sizing: I let conviction override sizing discipline.

Regime mismatch: I was bullish on Bitcoin but didn’t adjust for the fact that crypto miners have additional idiosyncratic risks

The addiction cycle:

Big wins trigger a dopamine rush

I immediately try to replicate it on the next few trades

When those trades go wrong, I double down in greater position size

I rationalized it: ‘I’m net positive.’ Technically true, but irrelevant—I was still violating my framework.

The results:

The lesson: Layering options (leverage) on individual miners (single-name risk) magnifies both tails. If I wanted Bitcoin exposure with convexity, I should have used a Bitcoin ETF like IBIT instead of miner options. I should also manage the position size.

The Scoreboard: Process Beats Prediction

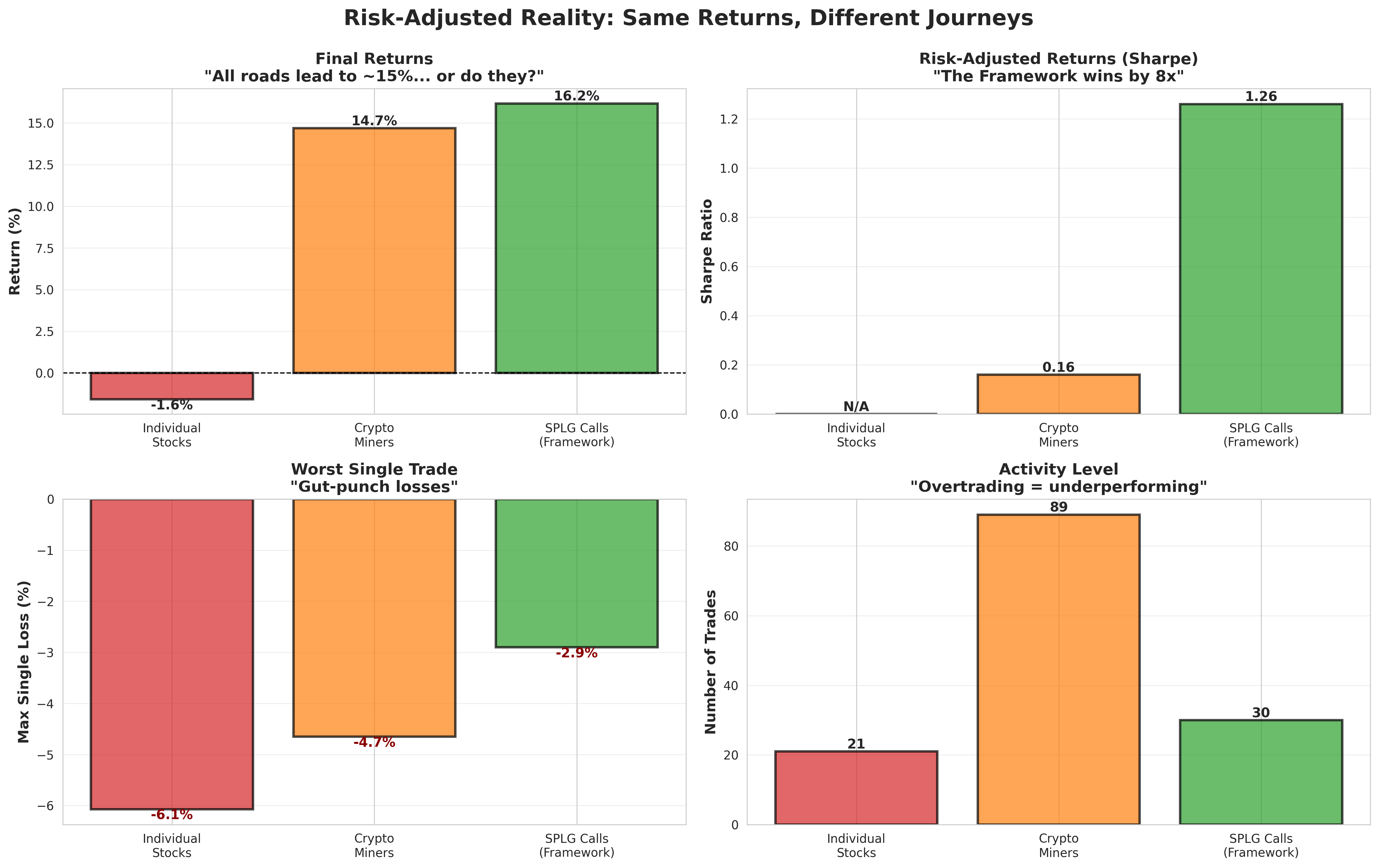

Here’s the final tally: Individual stocks lost 1.6%. Crypto miners made 14.7%. SPLG call spreads—the framework strategy—made 16.2%. On the surface, two of three made money, and the returns look similar.

But risk-adjusted returns tell the real story: Individual stocks: chaos with no reward. Crypto miners: Sharpe ratio of 0.16. SPLG: Sharpe ratio of 1.26—8x better!

Crypto miners: 89 trades over 18 months, max loss -4.6%, 65% of trades spent underwater. SPLG: 30 trades over 3 months, max loss -2.9%, steady capital growth

Bottom Line: The framework approach (SPLG index fund + options) delivered similar absolute returns with one-third the trades, half the max loss, and lower volatility.

(1) My edge is regime allocation and risk budgeting—not company analysis. When I stick to the process: asymmetric returns, manageable drawdowns. When I don’t: stress, chaos, and losses.

(2) Process beats prediction. Discipline beats dopamine. Boring beats exciting.

(3) Everything else—including my mistakes—is noise.

APPENDIX:

A. How the Regime Model Works

I monitor growth and inflation trajectories, then classify the macro environment into four quadrants. I corroborate with sentiment, earnings breadth, and market internals (trends, volatility, leadership).

Four Quadrants

Risk-on: Growth stable/improving, inflation contained/falling, spreads calm, earnings breadth widening, price above medium-term trend.

Playbook: Overweight equities; optional call spreads to lift beta; modest BTC sleeve; duration neutral/slightly short; gold neutral.

Risk-off (inflationary): Growth deteriorating, inflation elevated, real yields volatile.

Playbook: Reduce equity; raise gold; hold more short duration; options used for downside hedges; BTC minimal.

Risk-off (deflationary): Growth falling, inflation increasing rapidly, credit tightening.

Playbook: Cut equity beta; long duration; gold neutral/slightly long; no leverage; consider collars.

Transition/uncertain: Conflicting signals, rising dispersion, whipsaw risk.

Playbook: Tight bands, smaller options overlays, wait for confirmation.

Signals are ensemble-based; no single indicator drives the bus. I’d rather be approximately right with posture than precisely wrong with forecasts.

Options Overlay: Leverage With Guardrails

In risk-on:

Call spreads on equity indices with defined max loss (SPLG calls—worked perfectly when disciplined)

Occasional put overwrites on core equity (when vol is rich and risk is benign) to harvest carry

In risk-off:

Put spreads or collars to set floors

Little to no net long optionality unless it cheaply defends left-tail risk

When I violated this: May 2025 naked puts—paid premium without offsetting income

Always: Premium budgeted; position greeks monitored; no naked short convexity.

B. Operating Principles Checklist

Define the game: I seek regime mispricings, not security mispricings.

Violated by: FRCB, RIOT, HUT individual bets

Keep it liquid: If I can’t exit in stress, I shouldn’t size it big.

Violated by: FRCB options, oversized crypto miner positions

Codify decisions: Indicators, thresholds, and bands live in writing.

Followed well: SPLG campaigns had clear entry/exit rules

Violated by: Same-day reversals, panic hedges

Cap convexity: Options exposure is budgeted; no naked short volaltility

Followed well: SPLG call spreads were sized properly

Violated by: Oversized crypto miner calls

De-risk mechanically: Max drawdown triggers are pre-set.

Saved me: Got stopped out of overlays in May 2025 before bigger losses

Re-risk cautiously: Require multi-signal confirmation.

Followed well: Scaled into SPLG calls as signals confirmed

Violated by: Panic-bought puts on single credit signal

Cost matters: Every bps saved compounds.

Vindicated by: Low-cost SPLG vs. higher-friction individual stock trades

Review errors: Quarterly attribution and “what failed” memos.

This blog post is that memo.

Don’t chase late: If I missed the first inning, I don’t buy the ninth.

Violated by: Same-day reversals, late entries into volatile moves

Survive first: Return of capital before return on capital.

Violated by: FRCB (lost 100%), RIOT (lost >100% on some positions)

What is your Sharpe ratio?