Weekly Macro Update: Aug 20th, 2024

Mostly positive data (inflation, consumer activity, labor); some negative data (industrial production and housing)

TL;DR

Past Week

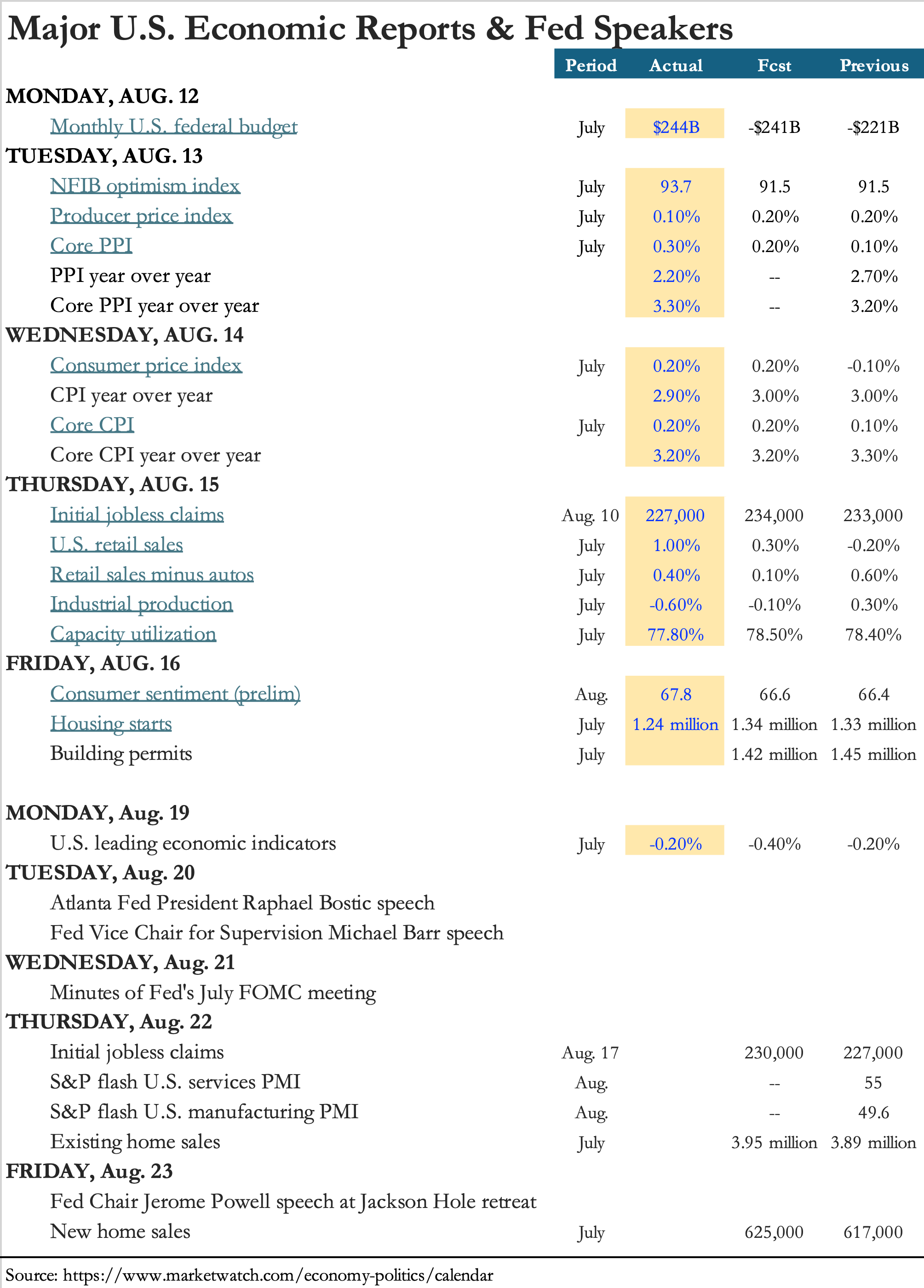

Positive data on inflation, consumer activity, and the labor marketInflation: Both the Producer Price Index (PPI) and Consumer Price Index (CPI) came in lower than expected, indicating that inflationary pressures are easing. This is good news for consumers.

Consumer activity: The retail sales figures significantly beat estimates and consumer sentiment improved, suggesting the US consumer is resilient.

Labor market: The lower-than-expected weekly initial jobless claims was positive. However, the slight increase in unemployment and decrease in non-farm payrolls could indicate the beginning of a cooldown.

Negative data on the industrial sector and housingIndustrial sector: Both capacity utilization and industrial production came in lower than expected, suggesting a potential slowdown in manufacturing and industrial activity.

Housing market: The housing sector appears to be cooling, with both building permits and housing starts coming in below estimates. This could be a response to higher interest rates and affordability concerns.

This Week

Federal Reserve Speeches (Tuesday to Thursday, Aug 22nd - 24th)

Federal Reserve's economic policy symposium in Jackson Hole, Wyoming

Initial Jobless Claims (Thursday, Aug 22nd)

Watch if reading is below estimates of 230K

Company Earnings Releases

Would you mind sharing this with your friends and colleagues? Every bit helps!

Macro Scorecard

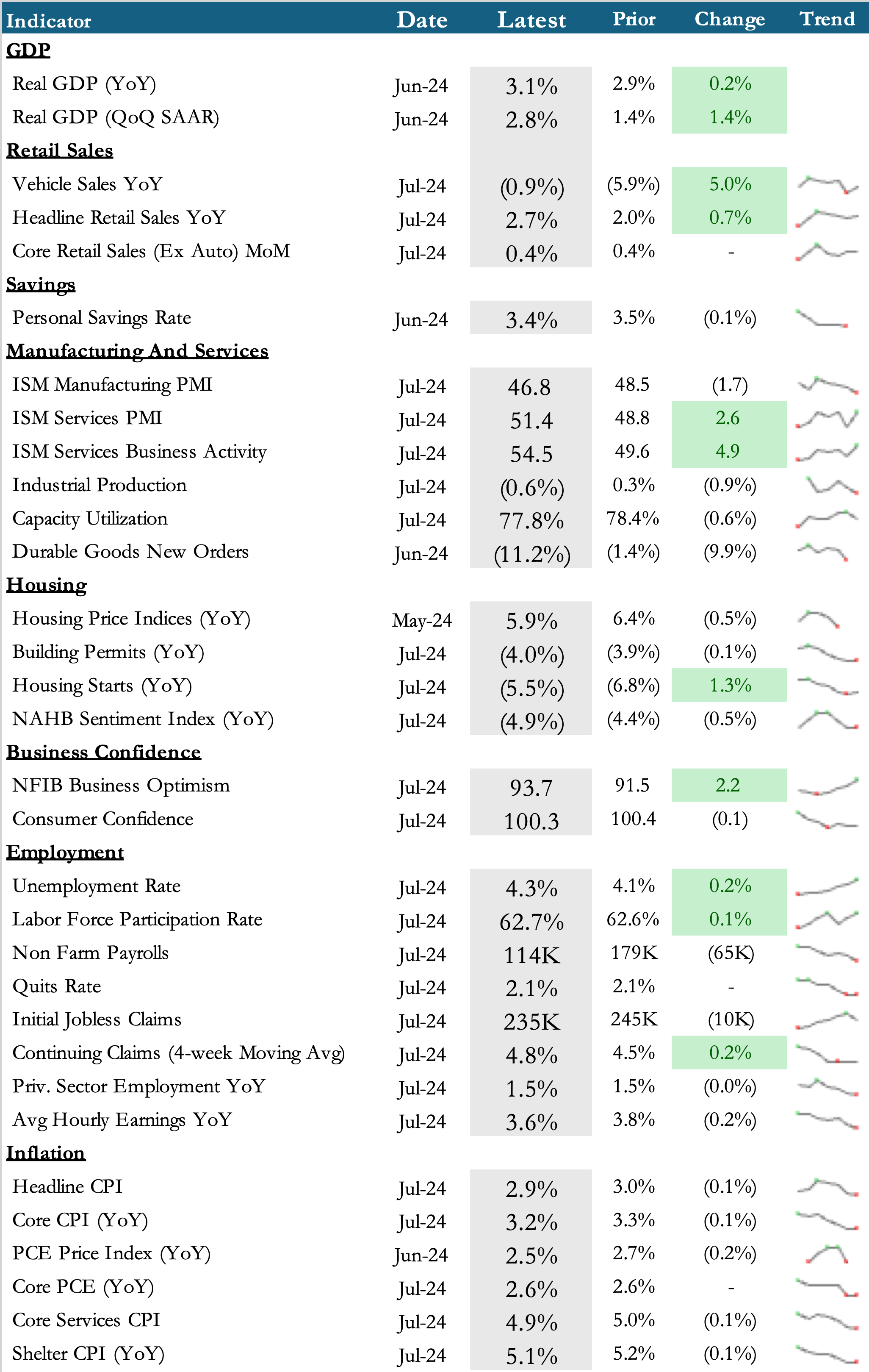

The mix of positive indicators (GDP growth, retail sales, services, sentiment) and negative signals (manufacturing contraction, housing slowdown) shows the economy is decelerating but not yet contracting.

Late Expansion Phase with Signs of Moderation: The economy appears to be in the late stages of expansion, but with signs of moderation:

GDP growth remains positive (3.1% YoY), indicating ongoing expansion.

Retail sales are growing, albeit at a modest pace.

The labor market remains strong with low unemployment (4.3%), though there are signs of cooling with a slight uptick in the unemployment rate and slower job growth.

Potential Transition to Early Slowdown: Some indicators suggest we might be transitioning towards an early slowdown:

Manufacturing PMI below 50 (46.8) indicates contraction in the manufacturing sector.

Industrial production has declined (-0.6%), suggesting softening in the industrial sector.

Housing starts and building permits are down year-over-year, pointing to a cooling housing market.

Mixed Signals in Services and Consumer Confidence:

The services sector remains in expansion (ISM Services PMI at 51.4)

Business optimism has improved slightly, while consumer confidence remains stable but high.

Inflation Moderation (Disinflation):

Inflation indicators (CPI, PCE) show a gradual decline, suggesting that monetary policy tightening may be having its intended effect.

Labor Market Resilient with Early Signs of Softening:

The job market remains strong overall, but the slight increase in unemployment and decrease in non-farm payrolls could indicate the beginning of a cooldown.

Shelter inflation still elevated (e.g. the shelter index increased 5.1% YoY, accounting for over 70% of the total 12-month increase)

Monetary Policy:

With inflation moderating and some signs of economic softening, the Federal Reserve might be nearing the end of its tightening cycle.

Markets are pricing in 4 rate cuts (by December) with a 74% probability

Economic Releases This Week