Can the market maintain its altitude?

Yes, but valuations are steep (altitude is high) so liquidity (fuel) is required

TL;DR

Borrowing Cem Karsan’s framework:

Karsan uses an analogy of a jet. Market flows—driven by factors like Fed policy and liquidity—often overshadow valuations and serve as “fuel” to pump markets higher in the short term. However, the higher you go (in valuations), the more tail risk there is. When flows reverse due to factors like seasonal effects ending, Fed policy changes, or other global events, fundamentals and valuations become more critical.

Why is this important?

Valuations are steep (altitude is high): One measure closely tracked by investors, the equity risk premium—the gap between the S&P 500’s earnings yield and that of 10-year Treasuries—shrank close to zero, the lowest level since 2002.

Strong fundamentals (airplane) and momentum (fuel) are driving markets: The economy has strong macro momentum and is essentially "full steam ahead" due to the Republican sweep (expect lower taxes and fewer regulations). However, this means that “fuel” (liquidity) is required to keep markets afloat. Any decrease in liquidity or increase in volatility (turbulence) may cause some pain.

Key questions answered this week include:

Growth: Will the U.S. maintain high levels of economic growth?

Inflation: Is inflation coming back higher?

Policy: Will the Federal Reserve maintain its dovish bias?

Liquidity: Will Chinese stimulus be successful in turning the economy around?

Answers:

Growth: Yes, although volatility could derail things (e.g., Ukraine, Nvidia, Trump cabinet picks)

Inflation: Yes, as evidenced by higher CPI, PPI, and retail sales. This serves as a tail risk.

Policy: Yes (for now), as evidenced by Powell’s press conference.

Liquidity: Probably not, but they will keep trying (liquidity positive) because they need to

Conclusion:

Despite elevated asset prices, the combination of strong economic momentum and accommodative monetary and fiscal policy creates a generally favorable environment for risk assets in the near term. I am planning to keep my hedges in place (bought puts last month) as inflation fears are re-emerging (see below), and markets fell last Friday. If markets continue to plunge further, I might decrease my exposure to the index.

Growth: Will the U.S. maintain high levels of economic growth? [Yes]

Prior Assumption [October 24th, 2024]

Growth: A sequence of deteriorating leading indicators, particularly in housing, suggests the Fed may need to balance inflation concerns against growing economic headwinds.

New Evidence

Bull Case:

The economy has strong macro momentum and is essentially "full steam ahead" due to the Republican sweep in the election (expect lower taxes and fewer regulations). This is further represented by the price of Bitcoin, which has surged by nearly a third since the eve of the election. Key factors supporting growth are: 1) robust labor market; 2) strong nominal income growth; and 3) productivity enhancements.

Sentiment has turned positive: The share of investors who said they were bullish jumped to 49.8% this past week, while the share of those reporting a neutral sentiment dropped to the lowest level since 2022. About 40% of those surveyed said the U.S. election made them more optimistic about the market.

Evidence of labor hoarding, the decline in job openings relative to total employment and the divergence between openings and hires, suggests employers are retaining workers due to challenges in rehiring and retraining.

Nominal employee compensation, a broad measure of income growth, remains well above trend, growing at 6.4% year-over-year.

Productivity has seen a notable increase, potentially driven by the necessity for businesses to adapt in a tight labor market.

Bear Case:

Low volatility (VIX is around ~13) + lack of protective puts means investors aren't positioned for tail risks. There are some things that could derail the market:

Geopolitical tensions: The US is approaching a final decision to lift some restrictions on Ukraine’s use of Western-made weapons to strike limited military targets in Russia. This could cause some volatility

Nvidia (NVDA): They have faced some challenges with the design of server racks for the new Blackwell graphics chips. The company already hit engineering snags in the development of its Blackwell chip lineup, slowing the release by at least a quarter. Given its large concentration in the S&P and its upcoming earnings on Nov 20th, this could cause some issues and price volatility.

Trump cabinet picks: Trump’s appointment of Robert F. Kennedy Jr. as health and human services secretary pressured several stocks, including Moderna and Pfizer. Other cabinet picks have been met with some resistance as well.

Inflation: Is inflation coming back higher? [Yes]

Prior Assumption [October 24th, 2024]

Inflation: U.S. consumers’ inflation expectations for the next 5-10 years skyrocketed to 7.1% in October, the highest since 2011, suggesting that inflation concerns are becoming more entrenched.

New Evidence

Policymakers seem to be dismissing potential inflation concerns, but I am not so sure that inflation is behind us. Inflation remains a concern, with core inflation potentially rebounding and wage growth showing signs of picking up, which could lead to a resurgence in inflationary pressures.

We saw higher CPI, PPI, and retail sales reports recently, but the threshold for evidence of reaccelerating inflation needed to change the Fed's policy trajectory appears to be extremely high. St. Louis Fed President Alberto Musalem noted that while the 2% inflation target is within sight, recent data have raised the risk that progress may slow or reverse. There is a risk that they may maintain an overly accommodative stance for an extended period, potentially reigniting inflation.

Wage growth, as measured by average hourly earnings (AHE), has been rebounding across private industries, service-providing industries, and goods-producing industries. The Indeed Wage Growth Tracker also points to a potential rebound in wage growth, with both the 3-month average and year-over-year growth rates trending upward.

The US consumer has not been significantly slowed down by the Fed's rate hikes, as evidenced by the sustained positive contributions of personal consumption expenditures to GDP.

Fiscal/Monetary Policy: Will the Federal Reserve maintain its dovish bias? [Yes—for now]

Prior Assumption [October 24th, 2024]

71% of major central banks are easing monetary policy, with the European Central Bank (ECB) and Bank of England cutting rates as expected. However, the U.S. is an outlier due to its above-average growth and rampant fiscal spending, which is causing inflation fears to re-emerge.

New Evidence

The normalization of interest rates by the Federal Reserve to around 3% is expected to provide a significant boost to both GDP growth and inflation over the coming years. This is liquidity positive, but rate cut expectations have declined meaningfully this week

In a speech on November 14, 2024, Powell emphasized that the Fed is "not in a hurry" to cut interest rates further, citing a strong economy and uneven progress in reducing inflation. However, he did characterize the current monetary policy as "restrictive", indicating that it is exerting downward pressure on economic activity and inflation. The sustained growth of the US economy (seven consecutive quarters of >2% growth) suggests that the policy may not be as restrictive as intended.

Liquidity: Will Chinese stimulus be successful in turning the economy around? [Probably not, but liquidity positive]

Prior Assumption [October 24th, 2024]

China’s Economic Challenges = Incremental Liquidity: China’s Q3 GDP grew by 4.6% year-over-year, the slowest pace in six quarters, impacting global demand. In addition to slower GDP growth, China’s debt-to-GDP ratio reached 366% in Q1 2024, indicating rising financial risks. There have been two consequences: new lending facilities to prop up markets (liquidity positive) and accelerating capital outflows.

New Evidence

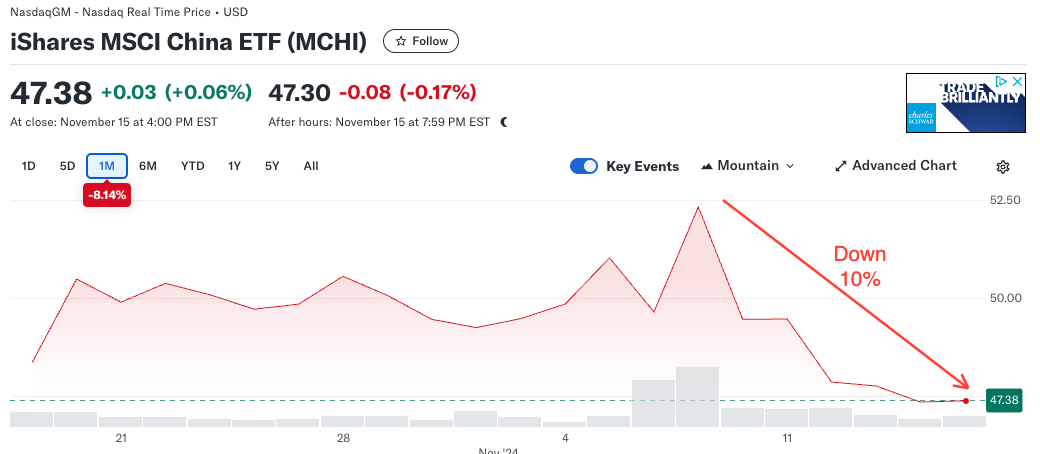

The MSCI China Index has fallen about 10% from a recent peak as excitement over the prospect of more government support for the market recedes and Donald Trump’s victory raises concerns over higher tariffs on China.

The election of President Trump heightens the urgency for China to stimulate its economy amid potential trade tensions. Trump on the campaign trail said he would raise tariffs on all Chinese imports into the U.S. to 60%, a move aimed at narrowing the U.S.’s yawning trade deficit and rebuilding American manufacturing.

Last week, China announced a $1.4 trillion plan (10 trillion yuan) to help cash-strapped local governments manage their debts. A significant portion of the funds is allocated to repaying "hidden debts" accumulated via local government financing vehicles (LGFVs).

Chinese industrial production slowed slightly in October and the real-estate sector remained in a deep slump, data published Friday showed. This further emphasizes the need for more stimulus measures.